- Samsung Beats Nvidia on Profit: The Truth Behind Record Profitability

- Samsung's Memory Chip Business is Doing All the Heavy Lifting

- How AI Memory Demand Is Driving Samsung’s DRAM, NAND and HBM Growth

- Why Samsung’s Record Earnings Failed to Fully Convince Investors

- Samsung Stock Analyst Ratings, Valuation and Outlook

- Is Samsung Stock Undervalued? A Valuation Analysis

- Samsung HBM Market Share vs SK Hynix and Micron

- Five Risks to Samsung’s AI Memory and Earnings Outlook

- Verdict on Samsung Stock: What Investors Should Watch Next

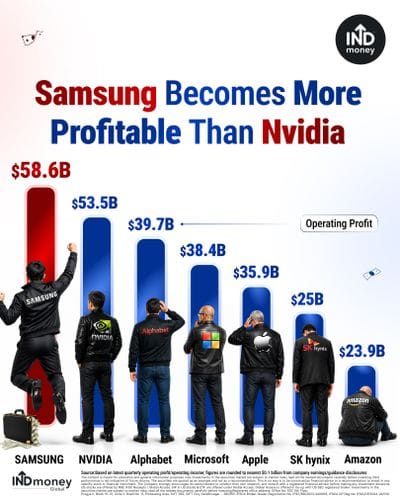

Samsung, a Korean electronics company just posted one of the largest quarterly operating profits forecast ever reported by a listed tech company. In the three months ending June 30, 2026, Samsung Electronics reported 89.4 trillion Korean won in operating profit, roughly $58.6 billion, exceeding Nvidia's most recent quarterly operating income of $53.5 billion.

Samsung earned more in this single quarter than it did across the combined three-year stretch of 2023, 2024, and 2025. Revenue hit 171 trillion won, up 129% from the same quarter last year. Operating profit jumped 1,810% year on year. And then, on the day Samsung released these numbers, its stock dropped roughly 7%.

Let's break down what actually drove this historic operating profit, why the market sold a record print, what Samsung's Q2 guidance tells us about the AI economy, whether this profit level holds, and what it means if you are tracking this story from India.

Samsung Beats Nvidia on Profit: The Truth Behind Record Profitability

Samsung's preliminary Q2 2026 earnings guidance filed with Korean regulators on July 7 show that the company’s operating profit, meaning earnings from core operations before taxes, interest, and non-operating items, came more than that of Nvidia, Google and even Microsoft and Apple.

Note that operating profit is not net profit; Nvidia's net income for the same recent period was approximately $58.3 billion, nearly identical to Samsung's operating profit, which illustrates why the metric matters for like-for-like comparisons.

Samsung’s Q2 profit also includes a large employee bonus expense linked to a labour agreement signed in May. Under the agreement, around 10.5% of the semiconductor division’s operating profit will be paid as special bonuses. Industry estimates suggest Samsung may have set aside about 15 trillion won for the first half of the year, although the company has not officially confirmed the amount.

Some local industry estimates suggest operating profit before these provisions would have exceeded 100 trillion won, but this is not an official adjusted figure from Samsung.

Samsung's operating margin for Q2 came to approximately 52.3%, up from 42.8% in Q1. Per Citi Research estimates, average selling prices for DRAM rose approximately 44% quarter on quarter in Q2, and NAND flash prices rose approximately 53% quarter on quarter. Those two numbers explain most of the margin expansion.

Samsung's Memory Chip Business is Doing All the Heavy Lifting

Samsung officially reports results across four segments:

- Device eXperience (DX), which covers smartphones, TVs, and appliances

- Device Solutions (DS), which houses memory, foundry, and System LSI;

- Samsung Display (SDC);

- Harman International, the audio and connected car unit.

The DS segment, specifically its memory business, is where Q2's extraordinary result came from. Samsung does not break out divisional earnings in its preliminary guidance filing, so the figures below are analyst estimates, not confirmed segment results. They will be disclosed when Samsung releases full Q2 results on July 30.

| Segment | What It Does | Analyst Estimate for Q2 2026 |

| Device Solutions (DS) | DRAM, NAND, HBM; also foundry and System LSI | Estimated to account for the overwhelming majority of group operating profit |

| Device eXperience (DX) | Smartphones, TVs, Home Appliances | Analysts expected severe margin pressure from higher memory procurement costs; operating loss possible but unconfirmed |

| Samsung Display (SDC) | Display panels for mobiles and other devices | Positive contribution, magnitude unconfirmed |

| Harman International | Audio and connected car technology | Stable, smaller contributor |

Source: Korea Investment & Securities, analyst consensus estimates. All figures are estimates pending Samsung's July 30 detailed results.

Think of it like a conglomerate where one division is printing cash while the rest are either treading water or paying above-market input costs because that same division's success pushed up raw material prices industry-wide.

For Indian investors, the closest structural parallel runs through Reliance Industries. Reliance did not build cars during India's automobile boom of the 2000s. It refined petroleum. But every car that rolled off any factory floor eventually needed petrol, and every petrol pump was buying from Reliance's refineries.

When car sales compounded at double digits, Reliance's refining margins compounded alongside them. Samsung today is doing the same thing for AI. It does not build AI models. It processes silicon into the memory that every AI engine must consume to function. The AI companies get the headlines; Samsung collects the margin.

How AI Memory Demand Is Driving Samsung’s DRAM, NAND and HBM Growth

Most coverage frames Samsung as a commodity chip company that caught the AI wave at the right moment. That is partially accurate but misses the structural point.

Every AI model trained, every inference request answered, every GPU deployed, every data center built requires memory. Lots of it. And that memory has to come from one of three companies with meaningful scale in advanced memory manufacturing: Samsung, SK Hynix, or Micron.

The tollbooth gets more expensive as AI advances. High Bandwidth Memory (HBM), the specialised memory stacked directly alongside AI accelerators, typically sells at a significant premium to conventional DRAM per gigabyte, though the multiple varies by generation, contract size, yield, and packaging configuration.

Nvidia's current flagship Blackwell Ultra GPU carries eight HBM3E stacks per unit, with HBM representing a significant portion of the overall bill of materials, though Nvidia does not publish a component-cost breakdown and public estimates vary. Nvidia's next-generation architecture, Rubin, is expected to feature substantially higher HBM4 capacity and memory bandwidth than current Blackwell configurations.

The exact number of HBM stacks is not authoritatively published. What is confirmed is that Rubin uses HBM4 and that each successive GPU generation has demanded more memory bandwidth, not less. The deeper question is whether this tollbooth is permanent infrastructure or a cyclical pricing window. History says memory cycles always turn.

The counterargument this time is that AI demand for memory is not bounded by the number of human devices the way smartphone or PC cycles were. Every incremental AI deployment increases aggregate memory demand, and that pattern looks different from any prior cycle. Whether it is different enough to sustain current pricing is the central investment debate.

Why Samsung’s Record Earnings Failed to Fully Convince Investors

On July 7, 2026, Samsung released preliminary Q2 results showing an 1,810% operating profit surge. Its Korean-listed shares closed approximately 6.9% lower on the day, after falling as much as 10.1% intraday. The KOSPI fell 4.9%, triggering a circuit breaker. SK Hynix fell approximately 6%.

There are three reasons the market sold a record print, and all three are worth understanding.

- The record profit was already priced in: Samsung’s shares had risen about 150% in 2026, while operating profit of 89.4 trillion won only modestly beat LSEG’s 87.3 trillion won estimate. The result was strong, but not surprising enough to support another sharp rally.

- Memory strength is masking losses elsewhere: DRAM and NAND drove most of Samsung’s profit, but its foundry and System LSI businesses are still loss-making. Until those units recover, they will continue to dilute the earnings benefit from the memory boom.

- The pace of memory price growth may be cooling: Citi estimated DRAM prices rose 44% quarter on quarter in Q2, while TrendForce expects Q3 growth of only 13–18%. Prices are still rising, but the slowdown has raised concerns that the steepest part of the cycle may have already passed.

Samsung Stock Analyst Ratings, Valuation and Outlook

Despite the selloff, the analytical community's view on Samsung stock remains broadly constructive. The stock closed at approximately KRW 285,000 on July 10, 2026.

Source: JP Morgan Research Note, Citi, S&P Global Market Intelligence

JPMorgan's July 7 note flagged Samsung's forward PE of approximately 5.2 times (based on consensus 2026 earnings estimates) as significantly compressed relative to its own history and relative to Nvidia and SK Hynix.

Their view: the market is pricing in a severe earnings downturn, and if that downturn proves shallower or slower than expected, the stock has room to reprice upward.

The counter-position is equally coherent. Memory stocks rarely trade at historical PE averages during peak-cycle quarters because the market prices in the inevitable reversal. The 2017–2018 cycle produced the same apparent cheapness on forward earnings right before DRAM prices collapsed.

Is Samsung Stock Undervalued? A Valuation Analysis

The forward PE debate is the simplest entry point into valuation. Using a consensus FY2026 EPS estimate, here are the bear, base and bull case scenarios for Samsung stock.

| Scenario | Forward PE | Implied Stock Price Range | vs KRW 285,000 |

| Bear Case | 5x | KRW 275,000–300,000 | Approximately -4% to +5% |

| Base Case | 7–8x | KRW 385,000–480,000 | Approximately +35% to +68% |

| Bull Case | 12–13x | KRW 660,000–780,000 | Approximately +132% to +174% |

The forward EPS used is consensus for FY2026 at approximately KRW 55,000–60,000 per share, subject to revision depending on H2 memory pricing.

JPMorgan's December 2026 target of KRW 480,000 implies approximately 68% upside from the July 10 close. The analyst consensus mean target of approximately KRW 487,000 implies approximately 71% upside from the same reference price. The central variable is not the multiple. It is whether Q3 and Q4 DRAM and NAND prices hold.

If memory prices decelerate sharply, the forward earnings estimate that anchors all these PE calculations falls, and the implied upside figures compress accordingly. That is why the July 30 full results call and Q3 pricing guidance are the most important near-term catalysts for anyone tracking this name.

Samsung HBM Market Share vs SK Hynix and Micron

The HBM story requires precision, because the numbers here are often conflated in media coverage.

SK Hynix currently holds more than 50% of the global HBM market and is Nvidia's primary supplier for both HBM3E and the emerging HBM4 generation. Its Q1 2026 operating margin hit 72%, a figure that illustrates the premium profitability of dominant HBM positioning. Samsung sits at approximately 21–22% HBM market share, with both Samsung and Micron having recovered ground from even lower positions in 2025.

That gap matters commercially. HBM typically sells at a significant premium to conventional DRAM per gigabyte, though the multiple varies by generation, contract size, yield, and packaging configuration. Nvidia qualification determines which suppliers access that premium. Samsung's repeated difficulty qualifying HBM products for Nvidia's highest-volume GPU programmes over the past two years has cost it both revenue and the valuation premium that SK Hynix commands.

Three things that receive less coverage:

- Samsung’s conventional DRAM scale matters more than its HBM rank: Samsung held about 38% of the global DRAM market in Q1 2026, ahead of SK Hynix at 29%. With DRAM prices rising roughly 44% quarter on quarter in Q2, this larger exposure drove a major share of Samsung’s record profit.

- AMD gives Samsung a second HBM growth route: Samsung and AMD signed an MOU covering primary HBM4 supply for the MI455X accelerator. It is not a final contract, but it shows Samsung can grow in premium HBM even without displacing SK Hynix as Nvidia’s main supplier.

- HBM4 execution is now the key technology test: Samsung plans to use its own 4nm process for HBM4 base dies, versus SK Hynix’s reported use of TSMC’s 12nm process. The smaller node could improve performance and efficiency, but success will depend on yields, reliability, and timely customer qualification.

Five Risks to Samsung’s AI Memory and Earnings Outlook

The bull case rests on real data. So does the bear case.

- AI spending must stay elevated: Samsung’s memory boom depends on hyperscalers continuing to invest heavily in AI infrastructure. Any slowdown in data-centre or accelerator spending would quickly weaken demand for DRAM, NAND and HBM.

- Samsung still trails in premium HBM: SK Hynix controls more than 50% of the HBM market and remains Nvidia’s main supplier. If Samsung fails to qualify HBM4 for Nvidia’s Rubin platform, its gap in the industry’s highest-margin segment could widen further.

- Higher supply could end the pricing cycle: Samsung, SK Hynix and Micron are all expanding capacity. Since new DRAM production can take 24–36 months to reach meaningful volumes, investments made in 2025–2026 could pressure prices by 2027–2028.

- Foundry losses remain a structural drag: Samsung’s chip-manufacturing business continues to trail TSMC in advanced-node orders. Even if yields improve, it may take several quarters before foundry contributes meaningfully to group profit.

- Employee bonuses will absorb part of future profits: Samsung’s May 2026 labour agreement links employee incentives to semiconductor earnings. The Q2 provision was unusually large, but strong memory quarters will continue to carry higher labour costs, reducing the direct flow-through from operating profit to shareholders.

Verdict on Samsung Stock: What Investors Should Watch Next

Samsung's Q2 2026 result is not accidental. The 1,810% profit surge reflects a genuine change in the demand structure for memory: AI has made DRAM and NAND something closer to infrastructure than to consumer electronics components.

AI deployments cannot operate without memory, but purchase volumes remain sensitive to hyperscaler capital expenditure, deployment timelines, and memory pricing. That demand pattern is different from the smartphone upgrade cycle of 2017–2018, where saturation was eventually reached.

What is still not resolved is whether Samsung specifically is the cleanest way to express that view, given that SK Hynix captures the highest-margin HBM segment with greater efficiency, and that Samsung's foundry losses and mobile margin pressure dilute the purity of the memory thesis at the consolidated level.

Samsung's ordinary Korean shares are listed on the Korea Exchange but people who invest in US Stocks from India from apps like INDmoney can access stocks like Samsung through US-listed South Korean ETFs like iShares MSCI South Korea ETF (EWY) or Franklin FTSE South Korea ETF (FLKR).

What determines the next leg is Q3 memory pricing and Samsung's HBM4 customer qualification progress, both of which will become clearer on the July 30 detailed results call.