RateGain IPO subscribed 17.49 times so far: Read detailed review

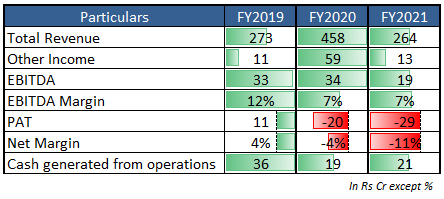

**RateGain Travel Technologies (RateGain) IPO which opened for subscription on 7th December, has seen strong subscription so far. The issue has been subscribed by 17.49 times at the end of 2nd day of the IPO. The company is looking to raise up to Rs 1,335.74 crore through the public issue. Here are the details:** ## About RateGain Travel Technologies IPO - **RateGain Travel Technologies IPO Date:** 7 December - 9 December 2021 - **RateGain Travel Technologies IPO Price band:** Rs 405 - Rs 425 - **Issue Size:** Rs 1335.74 crore (Fresh issue aggregating up to Rs 375 crore and offer for sale aggregating up to Rs 960.74 crore) - **Reservation:** QIB 75%, Retail - 10%, NII 15% - **Employee Reservation:** Rs 40 - **Minimum Investment:** Rs 14,875 - **Bid lot:** 35 shares, and in multiples of 35 shares ## Objectives of the issue - The net proceeds from the IPO will be utilized for the following purposes : - Repayment of indebtedness availed by RateGain UK (Rs 85.26crore) - Payment of deferred consideration for the acquisition of DHISCO (Rs 25.2 crore) - For strategic acquisitions and inorganic growth (Rs 80 crore) - Investment in tech innovation, AI (Rs 50 crore) - Purchase of capital equipment (Rs 40.7 crore) - General corporate purposes ## About RateGain Travel Technologies - RateGain Travel Technologies is one of the leading distribution technology companies globally. They are the largest Software as a Service (SaaS) provider in the hospitality and travel industry in India. - They offer travel and hospitality services to different verticals like hotels, airlines, online travel agents, package providers, meta-search companies, car rentals, cruises, and ferries. - It has served 1,462 customers as of September 30, 2021, including eight Global Fortune 500 companies - Its marquee customers include Six Continents Hotels, InterContinental Hotels Group, Kessler Collection, Lemon Tree Hotels, Oyo Hotels, and Homes Pvt Ltd. ## RateGain’s Products RateGain's products can be classified into three strategic business units: - **Data as a Service (DaaS)** - Under this product, the company delivers insights including competitive intelligence. The data is offered under two categories - - **Market Intelligence** - provides access to pricing and availability data at scale along with analytics to present trends, opportunities, and market developments. - **Dynamic Pricing Recommendations** - They serve certain segments within the travel industry that have traditionally used a flat pricing or a seasonal pricing structure with proprietary dynamic pricing technology to help them maximize revenue. - **Distribution** - They provide mission-critical distribution including availability, rates, inventory, and content connectivity between leading accommodation providers and their demand partners. - **Marketing Technology (MarTech)** – MarTech's offering enhances the brand experience to drive guest satisfaction, increase bookings, and increase guest loyalty. It also manages social media for luxury travel suppliers allowing them to be responsive to social media engagements 24x7 as well as effectively manage their social media handles and run promotional campaigns. ## RateGain’s Financials  - The revenue reported by RateGain for FY19, FY20, and FY21 is Rs 272.7 crore, Rs 457.61 crore, and Rs 264.09 crore, respectively. The revenue dropped in FY21 because of the pandemic. - The company has not posted profits in the last two financial years. In FY19, it posted a PAT of Rs 11.03 crore. In FY20 and FY21, it reported a loss of Rs 20.10 crore and Rs 28.58 crore. - For the last three financial years, RateGain has posted an average negative EPS of Rs (2.10) and an average negative RoNW of (9.42%). - The aggregate value of bookings completed using its products was Rs 62,858 crore, Rs 48,758 crore, and Rs 14,187 crore in FY19, FY20, and FY21, respectively. The average booking value was Rs 20,134, Rs 16,339 and Rs 15,732, in similar periods. - In FY19, FY20, and FY21, the company generated 34.65%, 35.06%, and 26.34% of its revenues from operations from the sale of services of transaction-based products. - It generated 30.07%, 40.86%, and 44.16% of revenues from operations from the sale of services of subscription-based products in the same period. ## RateGain’s Listed Peers There are no listed companies in India that engage in a business similar to RateGain. Hence, it is not possible to provide an industry comparison of the company. ## RateGain’s USP - **Long-term relationships with global customers** - The company has a global and diverse customer base with whom they have long-standing relationships. Its longstanding relationships with customers are evidenced by Gross Revenue Retention that is 92.78%, 95.46%, and 89.24% for FY19, FY20, and FY21, respectively. They offer customer support through their global support and implementation team that results in a quicker resolution of issues. They also have other customer-centric approaches that have ensured long-lasting relationships with their customers. - **Innovative AI-driven industry-relevant SaaS solutions** - They offer a comprehensive platform of industry-specific solutions with growth and monetization capabilities. They have developed products that are interoperable and integrate across a single platform allowing customers to maximize their revenues while also resulting in cost savings. The company continues to remain focused on developing applications that use data science, artificial intelligence, and machine learning. - **Diverse and comprehensive portfolio** - RateGain developed a comprehensive product portfolio that caters to the technology ecosystem for the hospitality and travel industry and in particular, to enterprise and mid-market customers for revenue management decision support, competitive intelligence, distribution, and social media marketing, online reputation and brand engagement. They are a market leader in social media solutions, and it is evident with the number of industry recognitions awarded to them. ## RateGain’s Growth Potential - **Continue to scale DaaS and Distribution offering** - They intend to leverage their portfolio of products and products under development to provide additional solutions to existing customers. The interoperability of its products allows them to displace point solutions and offer bundled offerings to customers. They plan to expand into adjacent verticals within the travel industry that relies on the same product set to guide their businesses. - **Focus on MarTech solutions** - Their strategy to grow the MarTech vertical is aimed at creating customer value at a time when guest traveler engagement with travel suppliers is being re-invented in the post-COVID-19 scenario. With the current dependency on third-party demand sources for bookings, hotels are keen to drive more direct bookings to help improve their earnings. They plan to leverage their proprietary marketing technology solutions to address this growing opportunity by offering its solution to large and luxury hotel chains. - **Continue to leverage unique data assets** - They are one of the largest aggregators of travel pricing data in the world. They use a data lake for storage and modeling travel-related data. To grow its product development capabilities, they have set up RateGain Labs, an in-house incubator that will leverage their existing expertise to solve current travel industry problems through data, proximity to clients, and business experience. - **Strategic investment and acquisition opportunities** - The company plans to selectively pursue strategic acquisitions and investments and other strategic alliance partnerships that are complementary to its growth strategy, particularly those that can help them enrich their offerings, enhance technologies and products, and expand customer base. ## RateGain’s Risks - **Revenue dependent on the worldwide hospitality and travel industry** - All of its revenues are derived from the worldwide hospitality and travel industry. The company's earnings are sensitive to factors affecting business volume in these industries. The worldwide hospitality and travel industry are highly sensitive to general economic conditions and trends. If travel volumes continue to be depressed or further decline because of the COVID-19 pandemic or any other factors, this could lead to a decline in the company's revenue. - **The decline in customer contract renewal** - It is essential for the growth and profitability of the company to maintain a strong relationship with its customers. The customers typically are not obligated to renew, upgrade, or expand their contractually agreed terms with them. Their ability to renew or expand customer relationships may decrease or vary because of many factors, including customers’ satisfaction or dissatisfaction with products and solutions, their reliability, etc. Under all such conditions, the company's revenue will be impacted. - **SaaS solutions in the hospitality and travel industry are new and evolving** - They generate, and expect to continue to generate, a large majority of their revenue from contracts in relation to SaaS products. The company believes that its success and growth will depend to a large extent on the widespread acceptance and adoption of SaaS solutions and DaaS, Distribution, and MarTech products. If this market develops more slowly than RainGate expectations or declines or develops in a way that they are not expecting, the business could be adversely affected. ## RateGain IPO: INDmoney Analysis RateGain's total revenues decreased by **43%** on-year to **Rs 264.09** crore in FY21, due to lower bookings in the travel and hospitality sector amid the pandemic. The company’s bottomline has also taken a hit from a profit of Rs 11 crore in FY19 to a **loss of Rs 30 crore in FY21**. The company said that it has healthy margins at the gross level, but the amortization of the cost of acquisitions and depreciation provisioning has resulted in a loss at net level. Due to its negative earnings, it is not possible to value the company on a PE ratio basis. At the higher end of the price band, RateGain IPO is priced at a Price to Book Value of ~**16.80 times (Apr- Aug 21)**. This seems to be aggressively priced. However, due to lack of peers and niche positioning, the company could command a scarcity premium. **Given the company’s leadership status as a SaaS provider in the hospitality space, healthy gross margins, strong runway for growth but aggressive valuations, investors with a higher risk appetite could consider investing in the issue. Risk of negative sentiments due to new variants of Covid could impact the prospects of the issue.** ## Subscription status as on 9th December 2021 (End of Day 3) | Category | Subscription (times) | |-----------|----------------------| | QIB | 8.42 | | NII | 41.05 | | Retail | 8.08 | | Employee | 1.36 | | Total | 17.49 |

What is RateGain IPO?

RateGain Travel Technologies is one of the leading distribution technology companies globally. They are the largest Software as a Service (SaaS) provider in the hospitality and travel industry in India.

How can I apply for RateGain IPO?

You can apply for RateGain IPO on the INDmoney app. Download the app from AppStore and PlayStore and apply using the app.

When can I apply for RateGain IPO?

RateGain opens for subscription on 7 December 2021 and closes on 9 December 2021.

What is the lot size?

You can apply for RateGain IPO in multiples of 35.

When will RateGain IPO allotment happen?

The finalization of the Basis of Allotment for Shriram Properties IPO will be done on Dec 14, 2021.

When is RateGain going to get listed?

The exact date is not available. The tentative date for listing is 17 December 2021.